If your organization is scaling AI adoption, you're probably asking: What does this mean for the rest of our software stack?

It's a practical question. AI platforms are consuming a growing share of software budgets, and finance and procurement teams need to understand which existing tools are most likely to face scrutiny at renewal time.

To answer this, we analyzed anonymized spend data from over 1,300 mid-market and enterprise companies through April 2026, comparing how the most AI-intensive organizations (what we are calling "AI early adopters") are allocating their project management software budgets versus their peers — and how those patterns differ between mid-market and enterprise.

Project management software is an interesting category to watch because it sits at the center of how teams plan, coordinate, and execute work. As AI tools become embedded across functions, there are competing theories about what should happen next. Some expect AI to automate enough routine work that organizations can reduce spending on traditional project management tools. Others argue that managing AI-powered workflows will increase the need for coordination, visibility, and cross-functional planning. This spending data offers an early look at which of those forces may be winning.

For this analysis, we honed in on Asana, Atlassian, and monday.com — three of the largest project management platforms by market share.

If you're a finance or procurement leader, these findings have direct implications for how you plan renewals, negotiate contracts, and allocate budget across your software portfolio.

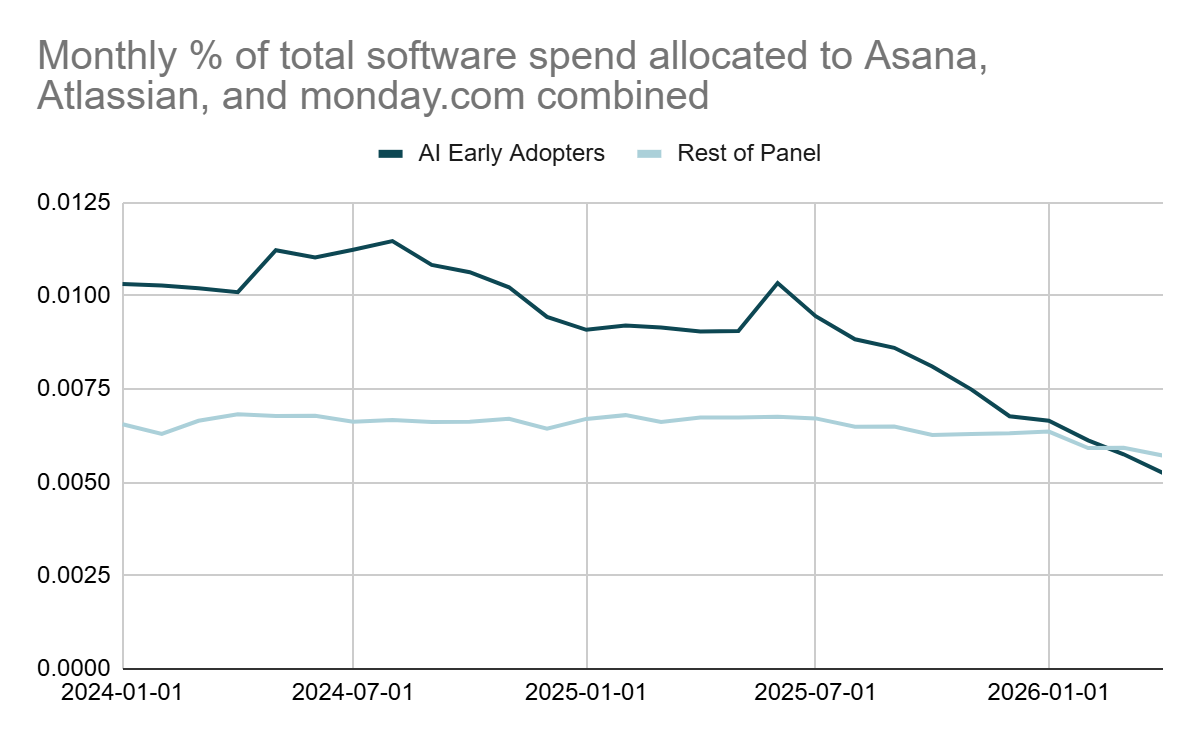

Among mid-market companies in our panel, the trend is clear and accelerating: AI early adopters are investing less in project management software. The total numbers aren't large, but directionally, the motion is clear.

AI early adopters allocated 0.53% of their total software budgets to Asana, Atlassian, and monday.com in April 2026, down from 0.90% a year earlier. That's a 42% decline in budget share. For context, the rest of the panel also reduced PM allocation — from 0.67% to 0.57% — but the decline was more moderate at 15%.

The divergence has been widening steadily since early 2025 and continued through the first four months of 2026.

Exhibit 1 — Mid-Market PM Software Budget Allocation: AI Early Adopters vs. Rest of Panel (January 2024 – April 2026)

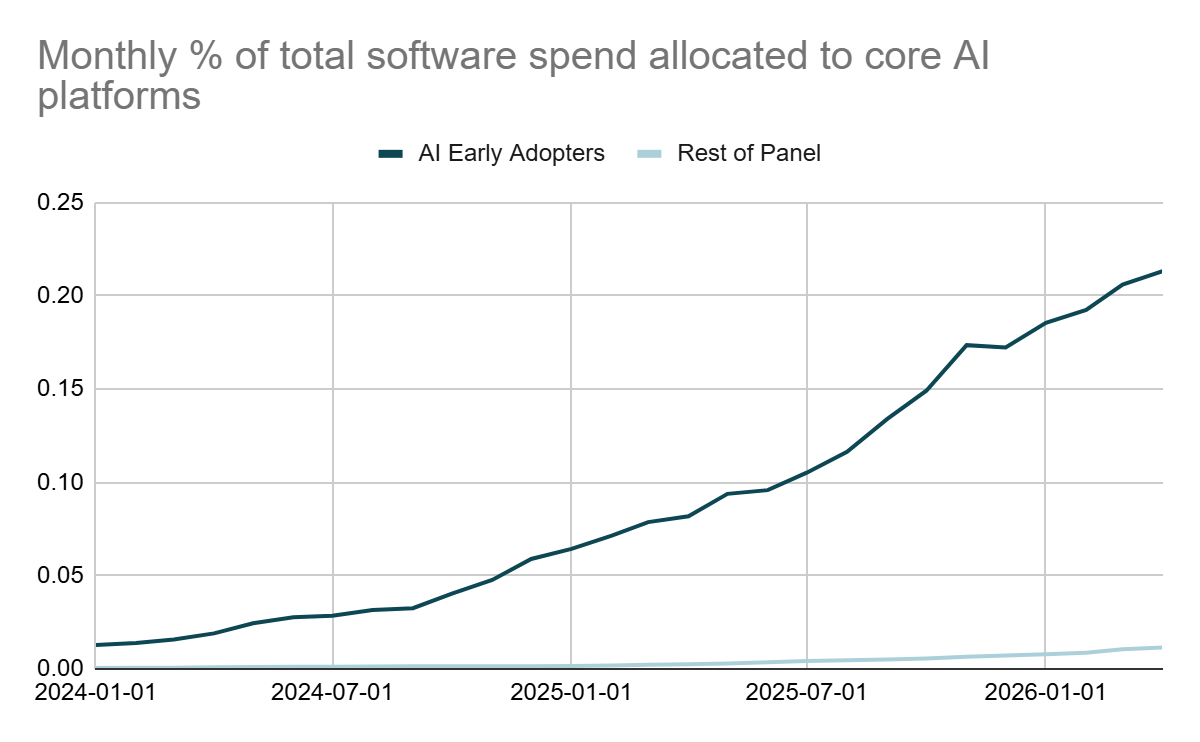

So what's driving this shift?

The math is straightforward: AI early adopters now allocate 21.3% of their total software budgets to core AI platforms, up from 8.2% a year ago. That's a 161% increase in AI's share of wallet.

Exhibit 2 — Mid-Market Core AI Budget Allocation: AI Early Adopters vs. Rest of Panel (January 2024 – April 2026)

When one category grows from 8% to over 21% of your budget in 12 months, every other line item shrinks as a percentage — even if its absolute dollar amount hasn't changed.

This matters because software budgets rarely expand at the same pace as emerging technologies. When a category grows from roughly one-twelfth of software spend to more than one-fifth in a single year, it begins competing directly with established software investments for budget.

In that context, the PM software findings become easier to understand. The question isn't necessarily whether organizations have become less dependent on project management tools. Rather, AI is becoming large enough that existing categories may need to justify their place in the budget more aggressively than before.

For finance and procurement leaders, relative budget allocation often influences future spending decisions. And categories that consistently lose share of wallet tend to face greater scrutiny during budgeting cycles, renewal negotiations, and vendor consolidation discussions.

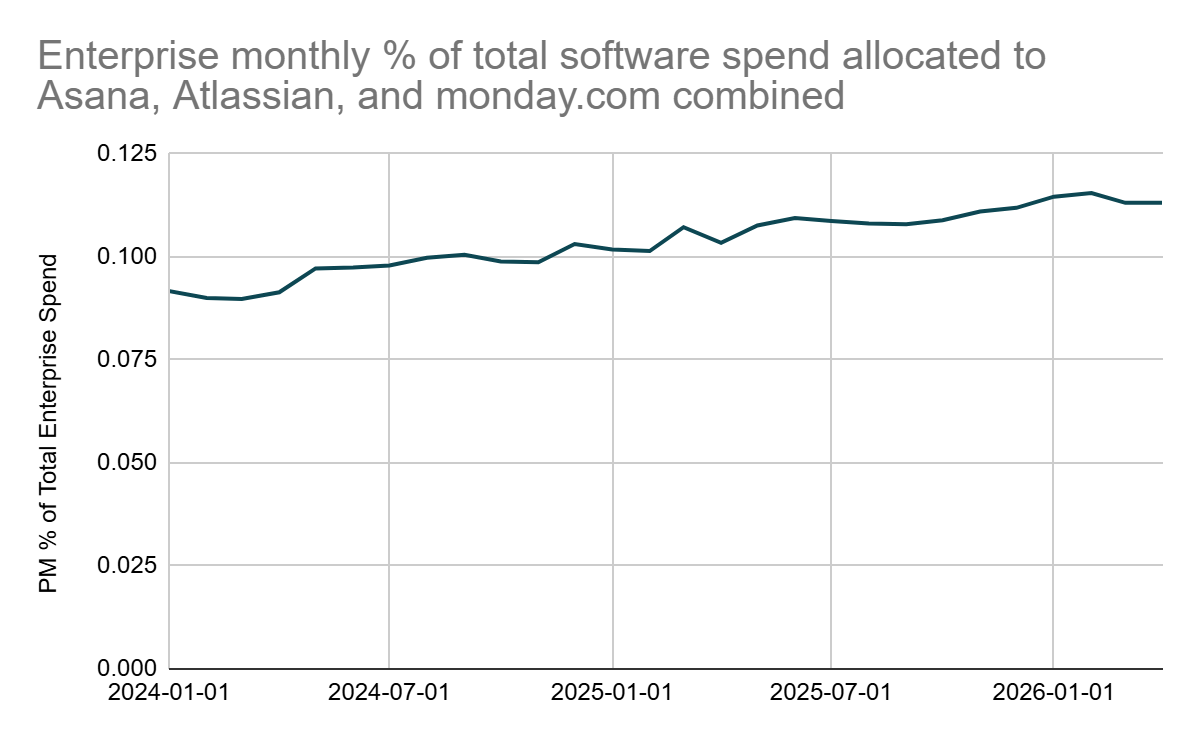

Importantly, this pattern is not universal. When we looked at enterprise organizations, we found the opposite dynamic: PM software is actually gaining share of total software budgets.

Across the 340+ enterprise companies in this analysis, the share of total software spend allocated to Asana, Atlassian, and monday.com grew from 9.2% in January 2024 to 11.3% in April 2026 — a 23% increase in budget share over 28 months.

Year-over-year, enterprise PM allocation grew from 10.3% in April 2025 to 11.3% in April 2026 — a 9.4% increase in budget share.

So, while AI-forward mid-market companies are deprioritizing PM tools, enterprise organizations are giving PM software a larger slice of their overall budgets.

While this analysis doesn't establish causation, the data suggests that enterprise organizations are continuing to expand PM software's share of wallet even as AI investment has accelerated. One possible explanation is that AI adoption creates additional coordination demands across teams, increasing the value of project management and workflow tools.

It's worth noting that enterprise PM allocation growth has plateaued slightly in early 2026: allocation was 11.19% in December 2025 and 11.31% in April 2026 — essentially flat over four months. While still well above year-ago levels, the deceleration is worth monitoring.

Exhibit 3 — Enterprise PM Software as % of Total Software Spend (January 2024 – April 2026)

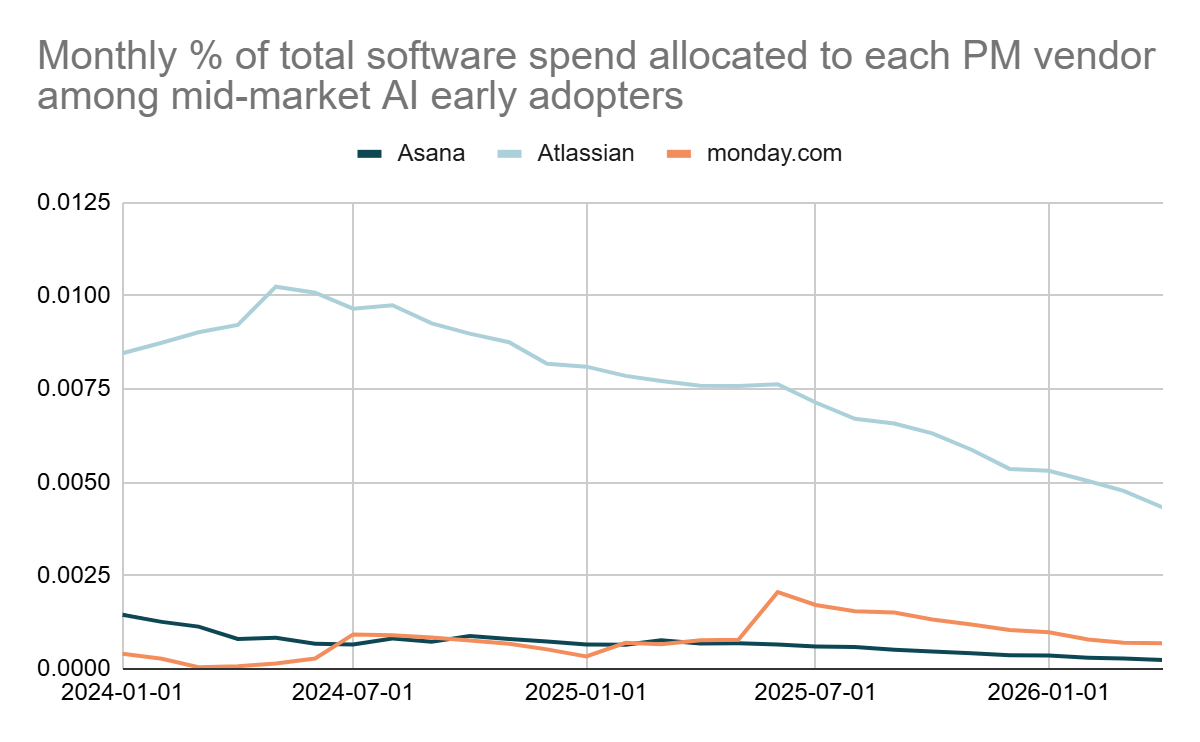

At a category level, the divergence between mid-market AI adopters and enterprise organizations is clear. But is the trend concentrated in a single vendor, or is it occurring across the broader project management software category?

Among mid-market AI early adopters, all three platforms saw declining budget allocation over time, though the magnitude varied.

Atlassian accounted for the largest share of PM software spending among AI early adopters throughout the period, reflecting its strong presence in engineering-focused organizations. Even so, Atlassian's share of software budgets among AI early adopters declined from 0.85% in early 2024 to 0.43% in April 2026.

(See actual pricing for Atlassian, from real contracts tracked in SpendHound.)

Asana experienced the largest proportional decline, falling from approximately 0.15% to 0.02% over the same period.

(See actual pricing for Asana, from real contracts tracked in SpendHound.)

monday.com followed a similar directional pattern, though its smaller allocation levels make month-to-month movements more volatile.

(See actual pricing for monday.com, from real contracts tracked in SpendHound.)

Taken together, the data suggests the mid-market shift is broader than any individual vendor. AI early adopters appear to be allocating a smaller share of software budgets to project management tools across the category.

Exhibit 4 — Individual Vendor Budget Allocation Among Mid-Market AI Early Adopters (January 2024 – April 2026)

If you're a finance or procurement leader evaluating PM software contracts, here are some next steps:

If your organization is scaling AI adoption, your PM software allocation may be declining as a share of total spend, even if you haven't actively cut it. Understanding where you sit relative to peers helps frame renewal conversations.

As PM software competes with a growing number of AI investments for budget, finance and procurement teams may have greater incentive to scrutinize seat utilization, contract structure, and overall ROI at renewal time. That increased scrutiny can create opportunities to negotiate more favorable pricing, right-size unused licenses, or revisit contract terms.

The data shows opposite trends by company size. Enterprise PM allocation is growing (+9.4% YoY), while mid-market AI early adopters are pulling back sharply (-42% YoY). Your renewal strategy should reflect your organization's size and AI adoption profile as well as other strategic business considerations.

With three major PM vendors showing similar trends, organizations running multiple tools may find consolidation increasingly attractive, particularly if — or when — more AI-native project management features begin to emerge.

The bigger story may not be what is happening to project management software. It may be what happens across the software portfolio when AI grows from 8% of budget to more than 20% in a single year.

Want to benchmark your software and AI spend against 1,300+ companies? Book a SpendHound demo.

Data source: Anonymized, aggregated software spend data from 1,300+ mid-market and 340+ enterprise companies, sourced directly from ERPs and enterprise data partnerships.

Time period: January 2024 through April 2026 (latest available data).

AI Early Adopter definition: Top mid-market companies by percentage of total software spend allocated to core AI platforms in April 2026, filtered to those with at least 2x year-over-year AI spend growth. This produced a cohort of 42 companies.

Core AI platforms: OpenAI, Anthropic, Anysphere (Cursor), Cohere, Mistral AI, Together AI, Fireworks AI, Hugging Face, Replicate Labs, Scale AI, Midjourney, ElevenLabs, Stability AI, and Perplexity.

PM vendors analyzed: Asana, Atlassian, and monday.com. All references to "PM software spend" in this analysis refer specifically to combined spend across these three vendors, not the full project management category.

Mid-market panel: Our mid-market panel includes over 1,300 companies with visibility into their software spending behavior. Of those, 42 qualified as AI early adopters based on the criteria above. The remaining 1,021 companies form the comparison group ("rest of panel").

Enterprise panel: Our enterprise panel includes 340+ companies. Note that enterprise data is presented at the aggregate panel level. Panelist-level cohort analysis (AI early adopters vs. rest of panel) is available for mid-market only.

Among mid-market AI early adopters, PM software's share of total budgets declined ~42% year-over-year by April 2026 — nearly 3x the rate of the broader panel. The pattern is deprioritization, not necessarily elimination: AI platforms are consuming such a rapidly growing share of total software budgets that PM tools are shrinking as a proportion of overall spend. For finance and procurement teams, this distinction matters: Deprioritization today often leads to harder renewal conversations tomorrow.

It depends on your company size and AI adoption profile. At the enterprise level, PM software's share of total budgets is actually growing, up from 10.3% to 11.3% year-over-year. For mid-market companies, budget allocation to PM tools is declining, especially among AI-forward organizations. Whether that translates to actual dollar cuts depends on how fast your overall software budget is growing.

Mid-market AI adopters show declining PM allocation, while enterprise organizations show modestly expanding PM allocation. This likely reflects the increased coordination complexity that comes with deploying AI at scale across large organizations.

According to SpendHound's benchmarking data, organizations investing heavily in AI are placing greater scrutiny on existing software budgets, particularly in the mid-market. As AI competes for a larger share of software spending, finance and procurement teams have even more reason to benchmark pricing, right-size licenses, revisit contract terms, and evaluate opportunities to consolidate project management tools before renewal.

YipitData's insights are powered by Signals, a proprietary B2B spend panel derived from anonymized ERP transaction data across 1,300+ mid-market and enterprise companies. This provides visibility into real software purchasing behavior across ~250,000 vendors — capturing momentum earlier than traditional signals like funding or headcount.

SpendHound, a subsidiary of YipitData, is a SaaS and AI spend-management platform that benchmarks pricing for 10,000+ vendors, tracks renewals, centralizes contracts, and helps companies reduce software costs by using real market data and expert negotiation support.

Book a demo below and we'll get you set up with our team.